What Determines Oil Prices?

Oil prices feel chaotic. They jump overnight after a news headline, drop for weeks with no obvious trigger, confound the experts and surprise the markets.

But underneath every move is a logic. Supply and demand set the floor and the ceiling. OPEC manages the middle. Geopolitics creates the spikes. Futures markets price in the future. And the energy transition reshapes everything over the long run.

Once you understand that logic, the number on the pump stops being a mystery and starts making sense. This guide explains exactly what drives oil prices using plain language, real examples, and the latest data from 2026.

1. Supply and Demand: The Foundation of Every Oil Price

Every oil price starts in the same place. It starts with the most basic rule in economics: supply versus demand. When the world produces more oil than it consumes, prices fall. When it consumes more than it produces, prices rise. Simple in theory. Complicated in practice.

Right now, the world produces an enormous amount of oil. World oil output is forecast to rise by 2.4 million barrels per day in 2026, reaching 108.6 million barrels per day total. That is a staggering volume. At the same time, demand is growing but more slowly. Global oil demand is forecast to rise by just 850,000 barrels per day in 2026, with non-OECD economies like China and India driving the entire increase.

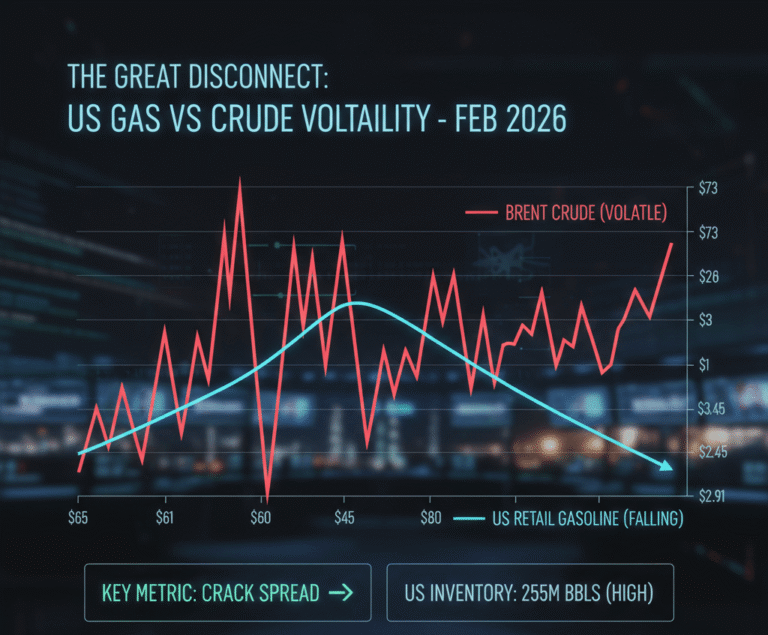

The gap between supply growth and demand growth matters enormously. When supply outruns demand, oil builds up in storage tanks around the world. Those inventory builds push prices down. The EIA forecasts that global oil inventory builds will average 3.1 million barrels per day in 2026 and as a result, Brent crude spot prices will average just $58 per barrel this year, down from $69 per barrel in 2025. More oil sitting in storage means less urgency to buy. Less urgency means lower prices.

Demand is not static either. Economic growth is one of the biggest factors affecting oil demand. Growing economies mean higher demand for energy, especially for transporting goods from producers to consumers. When economies expand, factories run harder, trucks drive further, and planes carry more passengers. All of that burns oil. When economies slow down or enter recession, demand drops and oil prices follow.

2. OPEC and OPEC+: The Group That Moves Markets

You cannot talk about oil prices without talking about OPEC. The Organization of the Petroleum Exporting Countries controls a massive share of global supply. And when OPEC speaks, markets listen.

OPEC’s oil exports

OPEC member countries collectively produce about 35% of the world’s crude oil. OPEC’s oil exports account for around 50% of all the oil traded internationally. That dominant share gives the group enormous leverage. When OPEC cuts production targets, global supply tightens. Prices rise. When it raises targets, supply increases. Prices fall. It is a deliberate, coordinated management of the world’s most traded commodity.

OPEC does not act alone anymore. It operates through OPEC+, a coalition that includes major non-OPEC producers, the largest of which is Russia. Oil prices are driven not only by current supply and demand, but also by expectations of future supply and demand. OPEC tries to adjust its production targets based on these expectations. That forward-looking element is critical. OPEC is not just reacting to today’s market. It is trying to shape tomorrow’s.

OPEC’s spare crude oil production capacity also influences global crude prices and serves as an indicator of oil market tightness. Spare capacity is defined as the volume of production that can be brought online within 30 days and sustained for at least 90 days. Think of spare capacity as a pressure valve. A large spare capacity calms markets, there is a buffer if something goes wrong. Low spare capacity makes markets nervous. Any disruption could spike prices immediately, because there is no cushion.

OPEC members do not always follow agreed targets, however. Despite OPEC’s efforts to manage production, its member countries don’t always adhere to agreed-upon production targets this non-compliance can affect oil prices. Iraq, Nigeria, and Kazakhstan have historically exceeded their quotas, adding barrels the market did not expect. That kind of internal friction is one reason oil prices never perfectly follow OPEC’s stated intentions.

3. Geopolitics: When Politics Becomes a Price Tag

Here is what makes oil pricing genuinely unpredictable. A spreadsheet can model supply and demand. No spreadsheet can model a war.

Geopolitical events and oil pricing

Geopolitical events are among the most powerful short-term drivers of oil prices. They create what traders call a “risk premium”, an extra amount baked into the price to account for potential supply disruption. The bigger the threat, the higher the premium. With the region’s proximity to major energy chokepoints, brief, geopolitically driven crude rallies are likely to continue but these should eventually subside, leaving soft underlying global market fundamentals.

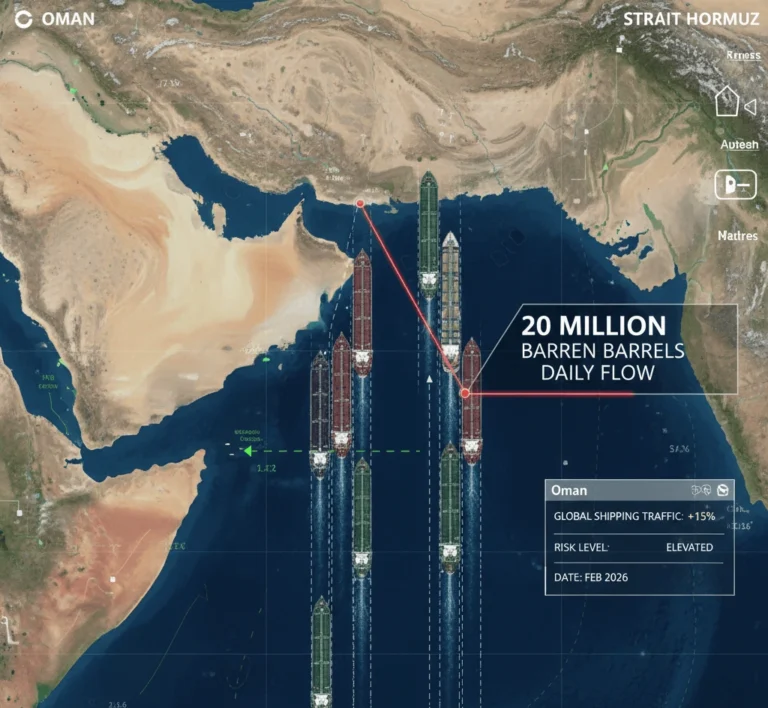

The Strait of Hormuz is the single most important chokepoint in the world. It is a 21-mile-wide passage between Iran and Oman. Every day under normal conditions, roughly 20 million barrels of crude oil pass through that narrow channel, approximately 20% of the world’s entire daily oil consumption. When tensions rise in the Persian Gulf, oil traders immediately price in the risk that those barrels might stop flowing. The price goes up before a single barrel is actually disrupted. That is the risk premium at work.

Sanctions add another layer of complexity. Sanctions on Russian oil are reshaping global trade flows, with barrels being redirected away from India and primarily toward China. When one major producer is cut off from normal markets, global trade routes shift. Buyers scramble to replace supply. Prices in some regions spike while discounted barrels pile up elsewhere. Sanctions do not remove oil from the world, they reroute it, inefficiently, at higher cost to everyone.

Geopolitics can quickly remove barrels from the market, and traders add a risk premium when shipping routes or production sites are threatened, disrupted shipping flows, especially around key chokepoints, represent volumes too large to replace quickly. That speed asymmetry is the crux of the problem. It takes years to build new production capacity. A missile can disrupt it in seconds.

4. Futures Markets and Speculation: The Price Before the Barrel

Most people assume oil prices reflect what oil costs today. They are wrong. Oil prices reflect what traders think oil will cost in the future. That distinction changes everything.

Oil futures markets

Oil is traded on futures markets, exchanges where buyers and sellers agree today on a price for oil delivered at a later date. The most widely watched benchmarks are Brent Crude (the global standard, priced in London) and West Texas Intermediate or WTI (the U.S. benchmark). These prices are set by millions of transactions happening simultaneously, involving oil companies, airlines, hedge funds, banks, and individual speculators. Oil markets are essentially a global auction, the highest bidder wins the available supply.

Speculation amplifies price moves in both directions. When traders expect a supply disruption, they buy oil futures aggressively. That buying drives up the futures price, even before any actual supply is lost. Conversely, when traders expect a supply glut, they sell futures. The price drops before the extra barrels reach the market. Futures markets provide information about the physical supply and demand balance as well as the market’s expectations — rising prices indicate that additional supply is needed, while falling prices indicate there is too much supply for current demand.

Oil pricing and Currency values

Currency values also play a role most people overlook. Oil is priced globally in U.S. dollars. When the dollar strengthens, oil becomes more expensive for buyers using other currencies. Demand from those countries falls. The oil price softens. When the dollar weakens, oil becomes cheaper in local currency terms, demand rises, and the price tends to move up. Traders watch the dollar index as carefully as they watch inventory data.

Seasonal patterns add another layer of predictability. Demand for heating oil rises in winter. Gasoline demand peaks in summer as Americans drive more. Refineries shift between heating oil and gasoline production seasonally. These patterns are well-known and priced into futures markets months in advance. A cold winter forecast in October can push heating oil futures higher immediately, even though the cold weather is still months away.

5. The Energy Transition: A New Long-Term Pressure on Prices

Something new is shaping oil prices in 2026 that did not exist a decade ago. The rise of electric vehicles, renewable energy, and serious government decarbonization policy is creating long-term downward pressure on oil demand and every serious oil forecast now accounts for it.

Oil alternatives

The emergence of alternative solutions on the demand side through electrification and renewable energy is beginning to temper long-term oil demand growth, even though oil remains dominant in the near term. The key phrase here is “near term.” Today, oil still powers over 90% of the world’s transportation. But the direction of travel is clear and oil producers know it.

That awareness is changing investment behavior. Oil companies face a difficult dilemma. Invest heavily in new production capacity that might not be needed in 20 years or hold back, keep supply tight, and maximize revenue from existing fields while demand is still strong. Energy consultancies warn prices could either collapse toward $40 with accelerated renewable adoption or surge past $100 if emission targets stall, these outcomes are framed as scenario risks rather than central forecasts. That enormous range tells you everything about how uncertain the long-term picture truly is.

The EIA projects global fossil fuel demand will peak by 2030, with Brent prices now expected to decline toward roughly $54 per barrel by 2027 under current policies. That is a meaningful forecast from the most credible energy data agency in the world. If accurate, it means the era of $80 or $100 oil as a baseline is ending replaced by a structurally lower price environment driven by supply abundance and gradually moderating demand.

Oil pricing and China’s role

China’s role deserves special attention. China is the world’s largest oil importer and one of the largest EV markets simultaneously. It has purchased more crude oil to place into strategic inventories, this buildup has acted as a secondary source of oil demand, softening the price decline that would otherwise result from large supply surpluses. China is strategically stockpiling cheap oil while it transitions its economy toward cleaner energy. That dual behavior, buying more oil now while building the infrastructure to need less oil later, is one of the defining market dynamics of this decade.

Oil pricing is not a mystery. It is a system. And understanding that system is the first step to making sense of the energy world.

For daily oil price data, market analysis, and energy news, visit fuelandoilcompany.com.