How Oil Prices Become the Fuel Prices You Actually Pay

You hear that crude oil is trading at $72 a barrel. A few days later, diesel at your local pump costs $3.40 a gallon. Jet fuel is spiking. Heating oil is up. You do the math and nothing adds up. That is because the price you pay for fuel is not crude oil. It is crude oil plus an entire industrial chain, refineries, pipelines, taxes, distribution networks, and market forces, stacked on top of each other between the oil well and your tank.

Understanding that chain is the key to understanding fuel prices. This guide walks you through every step, from the barrel of raw crude oil to the diesel pump, the jet fuel truck, and the heating oil delivery. No industry jargon. No spreadsheets. Just a clear, logical explanation of one of the most important pricing mechanisms in the modern economy.

1. The Barrel of Crude Oil: Where Every Fuel Price Begins

Every fuel product starts as crude oil. But crude oil is not fuel. It is a raw material, a dark, thick liquid pulled from the earth that cannot power an engine in its raw state. Before crude becomes useful, it needs to be processed. And that processing adds cost at every stage.

What Is Inside a Barrel of Crude?

A single barrel of crude oil contains 42 gallons of raw material. Refiners do not choose what is inside that barrel, nature does. Crude oil is a mixture of hydrocarbons with vastly different properties. Some hydrocarbons are light and volatile. Others are heavy and dense. The composition varies significantly depending on where the crude comes from.

Light, sweet crude, like WTI from Texas or Brent from the North Sea, is low in sulfur and rich in lighter hydrocarbons. It is easier and cheaper to refine into high-value fuels like gasoline and jet fuel. Heavy, sour crude, like Canadian oil sands or some Middle Eastern grades, contains more sulfur and heavier molecules. It requires more complex and expensive processing to produce the same clean fuels.

That quality difference matters directly to price. Light sweet crude commands a premium over heavy sour crude precisely because it costs less to refine and yields more of the high-value products the market demands. When you hear “Brent crude” or “WTI” quoted on the news, you are hearing the price of specific crude grades, each with a different yield profile and a different refining cost.

The Crude Price Feeds Everything Downstream

The EIA estimates that the cost of crude oil accounts for about 60% of finished gasoline costs and roughly 50% of finished diesel costs. That means when crude prices move sharply, fuel prices must follow eventually. The relationship is not instant. Refiners carry inventory. Contracts are priced in advance. But over any two-to-four week period, crude price moves pass through to refined product prices almost entirely.

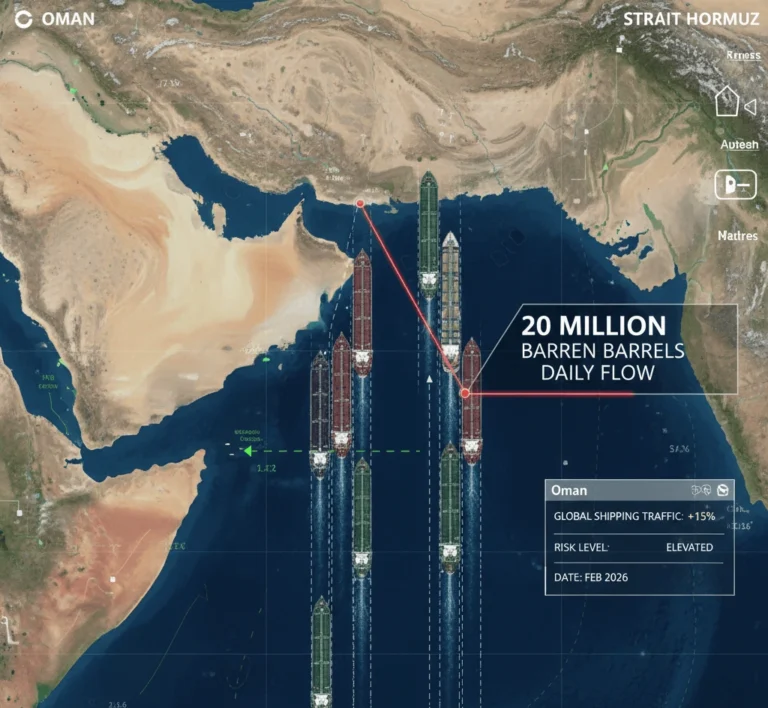

When crude spikes, as it did in early March 2026 following the Strait of Hormuz crisis, refined products follow within days. Diesel crack spreads in Europe surged to over $40 per barrel. Jet fuel premiums over Brent crude hit nearly $100 per barrel. The crude price move was the trigger. The refining system amplified it.

Crude Quality and Regional Differences

Not all regions process the same crude. U.S. refineries are heavily optimized to process light Permian Basin crude into gasoline and diesel. Middle East refineries produce relatively more kerosene and jet fuel. European refineries lean toward diesel production. Latin American facilities tend to produce more fuel oil and heavy products.

This regional specialization means that a crude price spike does not affect all fuels equally in all markets. A disruption to Middle Eastern crude supply hits jet fuel prices harder than gasoline prices, because Middle Eastern refineries supply a disproportionate share of global jet fuel. Approximately 23% of worldwide seaborne jet fuel trade passes through the Strait of Hormuz — making it uniquely exposed to Persian Gulf disruptions compared to other fuel types.

2. The Refinery: Where Crude Oil Becomes Usable Fuel

The refinery is where the transformation happens. Raw crude enters. Diesel, jet fuel, gasoline, heating oil, and dozens of other products come out. But the process is expensive, complex, and far from uniform.

How Refining Works: Cracking the Barrel

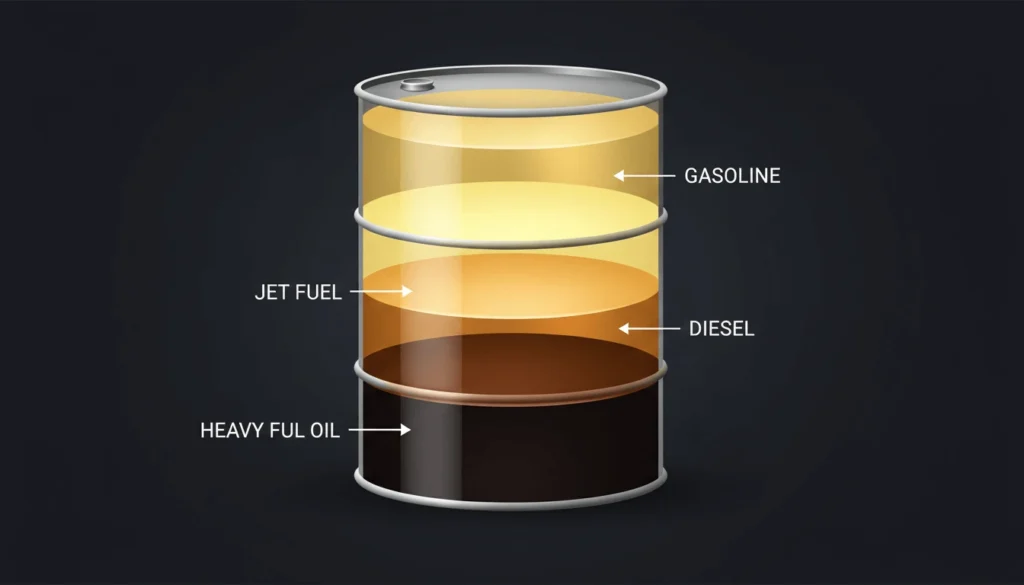

Refiners use a process called fractional distillation to separate crude oil into its component parts. They heat crude oil to extremely high temperatures inside a distillation column. Different hydrocarbons boil off at different temperatures and are captured at different heights in the column.

Lighter fractions, gasoline, naphtha, jet fuel, rise to the top and condense at lower temperatures. Heavier fractions, diesel, heating oil, fuel oil, settle lower in the column and condense at higher temperatures. The heaviest residual products sink to the bottom. Each fraction then goes through additional processing and treatment to meet the strict quality specifications that modern engines and aircraft require.

The word “cracking” in the industry refers to the additional step of breaking heavy hydrocarbon molecules into lighter, more valuable ones using heat, pressure, and catalysts. Fluid catalytic cracking (FCC) and hydrocracking are the two most common techniques. They dramatically increase the yield of high-value products, like diesel and jet fuel, from a given barrel of crude. A crack spread is typically calculated as the price of the refined product minus the price of the crude oil used to produce it.

Refinery Complexity and Its Cost Impact

Not all refineries are equal. A simple refinery can only do basic distillation. It produces a lot of low-value heavy fuel oil and relatively little high-value diesel or jet fuel. A complex refinery, equipped with FCC units, hydrocrackers, and cokers, can squeeze significantly more high-value product from every barrel of crude.

The market in 2026 is seeing a historic decoupling: crude prices remain suppressed by high production, yet the prices for diesel and jet fuel remain stubbornly high because the refining straw is too narrow to accommodate the flow. This structural bottleneck, too much crude, not enough sophisticated refining capacity, is one of the defining characteristics of today’s fuel market. Refiners with high-complexity scores capture the most value. Simple refineries struggle to compete.

The Geographic Migration of Refining Capacity

The global refining landscape is shifting dramatically. Between 2020 and 2024, more than 4 million barrels per day of refining capacity was shuttered in the West, while massive projects in the East faced pandemic-related construction delays. Now in early 2026, these delayed projects are arriving all at once. New mega-refineries in Kuwait, Oman, UAE, China, and India are coming online at scale. Meanwhile, aging European and North American refineries are shutting down under the weight of environmental regulations and high operating costs.

This geographic shift has real pricing consequences. European consumers now depend more heavily on imports of diesel and jet fuel from Asia and the Middle East. When supply routes are disrupted, as they were in early March 2026, European fuel prices spike faster and harder than markets with local refining capacity.

3. The Crack Spread: The Hidden Layer Between Crude and Fuel

The crack spread is the most important concept most fuel buyers have never heard of. It is the margin between what a refiner pays for crude and what it sells its products for. It is also a major component of the price you pay at the pump.

What the Crack Spread Measures

The crack spread tracks the difference between the spot prices for crude oil that refineries purchase and the spot prices for wholesale gasoline and diesel that refineries sell. It is the refiner’s gross margin before operating costs. It is called a “crack spread” because refining literally cracks crude oil into its component products.

The most widely used benchmark is the 3-2-1 crack spread. It represents the profit margin obtained by refining three barrels of crude oil into two barrels of gasoline and one barrel of diesel fuel. When this spread is wide, refining is profitable. Refiners run their facilities at maximum capacity. When the spread is narrow, refining margins are thin. Refiners slow down or cut back.

Why Crack Spreads Matter to You

Crack spreads are not just a trading metric. They directly influence how much fuel is available and at what price. When crack spreads widen, refiners produce more. Supply increases. Prices eventually moderate. When crack spreads narrow, refiners produce less. Supply tightens. Prices rise.

The crude surplus versus product scarcity paradox has defined the early months of 2026, keeping refining margins, or crack spreads, at a robust $8 to $12 per barrel, even as global oil demand growth settles into a post-pandemic steady state of approximately 930,000 barrels per day. That means even in an era of low crude prices, fuel products remain expensive, because the bottleneck is in refining, not in raw crude supply.

The Jet Fuel Crack Spread: A Special Case

Jet fuel crack spreads behave differently from diesel or gasoline spreads. Jet fuel is a middle distillate, similar to diesel but with tighter quality specifications. It competes with diesel for the same feedstocks inside the refinery. When diesel demand surges, jet fuel production can tighten. When jet fuel demand spikes, as it did during the post-COVID travel recovery, jet fuel cracks move independently of the broader crude market.

The price of jet fuel is notably high in 2026, commanding a premium over Brent crude of nearly $900 per ton, which translates to about $100 per barrel, as concerns about regional supply have led to the most significant changes in jet fuel crack spreads. Under normal conditions, the historical norm for jet fuel crack spreads is below $20 per barrel. A $100 per barrel spread is extraordinary and it illustrates just how sharply geopolitical disruptions can amplify fuel prices beyond what the crude price alone would suggest.

4. Taxes, Distribution, and the Last Mile: The Final Price Layers

Refined fuel leaving a refinery is still not the fuel you buy. It travels through an additional distribution system — and governments take a significant cut along the way.

Taxes: The Largest Single Addition in Many Markets

Fuel taxes are the most visible addition to the refinery gate price. They vary enormously by country and fuel type. In European markets, excise duties, VAT, and carbon levies can together represent 50% to 65% of the total retail price of diesel or gasoline. In the United States, combined federal and state taxes average around 50 cents per gallon for gasoline and slightly more for diesel. For jet fuel sold to commercial airlines, known as Jet A-1 internationally, most countries apply reduced or zero excise tax for international flights, which is one reason jet fuel at the refinery gate is often cheaper than retail diesel despite similar production costs.

These tax structures mean that a $10 move in crude oil prices does not translate equally to consumers in different countries. A $10 crude move represents a much larger percentage of the pre-tax fuel price in the U.S., where taxes are lower, than in France or Germany, where taxes are high and represent a larger fixed component of the price.

Pipelines, Terminals, and Storage

After the refinery, fuel travels through a distribution system before it reaches the end user. Pipelines carry large volumes of refined product from refinery clusters, like the U.S. Gulf Coast, to distribution hubs hundreds of miles away. From those hubs, the fuel moves to storage terminals. From terminals, tanker trucks deliver it to retail stations, airports, industrial facilities, and heating oil depots.

Each step in this chain has a cost. Pipeline tariffs are regulated but real. Terminal storage adds a fee. Truck delivery adds a significant per-gallon cost, one that rises when diesel prices rise, creating a feedback loop where higher crude prices make delivery more expensive, which pushes retail prices even higher. U.S. spot jet fuel supply and prices remain vulnerable to refinery issues, when a single large refinery faces an outage, regional supply shortages can push local jet fuel prices dramatically above the national average.

Marketing Margins and Retail Pricing

The final layer is the retail marketing margin, the profit taken by the fuel distributor or filling station operator. This margin is typically small in competitive markets, a few cents per gallon for gasoline or diesel. But it is not zero. And it tends to rise during periods of price volatility, when distributors need to compensate for the increased risk of holding inventory in a rapidly changing market.

Jet A-1 pricing for airlines works differently. Airlines do not buy fuel at retail. They negotiate directly with fuel suppliers and often purchase through long-term contracts or structured hedging programs. The price they pay is typically the spot market price plus a small into-plane fee, the cost of physically fueling the aircraft at the airport. That into-plane fee covers the airport fuel infrastructure, the fuel hydrant system, and the refueling staff. It varies significantly by airport and can add meaningfully to the cost of fuel in remote or infrastructure-poor locations.

5. What This Means for Diesel, Jet A-1, and Heating Oil in 2026

With the full pricing chain in view, the current fuel price environment in 2026 makes much more sense and is much more alarming.

Diesel: Caught Between Supply and Crisis

Diesel is the workhorse of the global economy. Every truck, train, ship, and generator runs on it. Its price affects the cost of every physical good transported anywhere in the world. In 2026, diesel faces a dual pressure. European refining capacity continues to shrink as old refineries close. Import dependency grows. And the Strait of Hormuz crisis has tightened middle distillate supply from the Gulf precisely when European storage is below seasonal norms.

The gasoil crack spread in Europe reached its highest point since August 2023, peaking at over $40 per barrel. Europe must cover its import needs even more heavily from the U.S., where diesel has also become significantly more expensive. The crack spread for U.S. diesel versus WTI has surged to approximately $70 per barrel, a figure that reflects both the logistical stress of rerouted supply and the underlying tightness of middle distillate markets globally.

Jet A-1: The Most Exposed Fuel of 2026

Jet A-1 is experiencing the sharpest price pressure of any fuel in 2026. The combination of strong air travel demand, constrained refining capacity, and direct supply route disruption through the Strait of Hormuz has created a perfect storm for aviation fuel prices. Airlines are facing a cost shock that they cannot immediately pass to passengers, existing ticket inventory is already sold. The pain lands first on operating margins and then, over months, on ticket prices.

U.S. jet fuel production averaged 1.815 million barrels per day over the first 11 months of 2025, with the refinery-rich Gulf Coast producing 958,000 barrels per day, more than all other U.S. regions combined. That concentration creates regional vulnerability. A single major refinery outage, like the fire at Chevron’s El Segundo facility in California in 2025, can spike West Coast jet fuel prices by 50 cents or more per gallon within days. In 2026, with geopolitical pressure added on top of operational risk, jet fuel price spikes are more frequent and more severe.

Heating Oil: The Consumer Cost Nobody Talks About

Heating oil is the least-discussed fuel in public energy conversations. But for millions of households across the northeastern United States and northern Europe, it is the most directly felt energy cost in winter. Heating oil is chemically similar to diesel, it is produced in the same refinery process, and its price moves in lockstep with diesel crack spreads.

When diesel prices rise sharply in winter, as they did in early 2026, heating oil prices follow immediately. Unlike electricity, which can be generated from multiple sources, heating oil consumers have no short-term alternative. They buy at the prevailing price or go cold. That inelastic demand is why heating oil prices can spike harder and faster than almost any other consumer fuel during supply disruptions.

The Full Picture: Why Fuel Always Costs More Than Crude

The journey from crude oil to the fuel you use passes through refineries, crack spreads, pipelines, taxes, distribution costs, and geopolitical risk premiums. Each layer adds cost. Each layer responds differently to market shocks. And each layer creates a buffer, or an amplifier, between crude prices and retail prices depending on the circumstances.

In 2026, every layer is adding cost simultaneously. Crude prices are elevated by geopolitical disruption. Crack spreads are wide because refining capacity is insufficient to meet demand. Distribution costs are rising because diesel prices affect delivery costs too. Taxes in Europe are unchanged, meaning consumers absorb every cent of the upstream increase.

The result is fuel prices that seem disconnected from the crude oil number on the news. They are not disconnected. They are just the product of a very long, very complex chain and right now, every link in that chain is under strain.

Stay updated on fuel prices, refining margins, and energy market analysis at fuelandoilcompany.com.